What Is a De Facto Tax — and Why It Matters in the Paid Parking Debate

A de facto tax is a charge the government labels as a “fee,” but which operates like a tax in real life. Courts do not rely on labels. They examine how a charge functions, who pays it, how avoidable it is, and what the money is used for.

This distinction matters in Florida because taxes typically require voter approval, while true regulatory fees or enterprise revenues often do not.

In the context of paid parking in Fernandina Beach, this question is not academic. It goes to the heart of whether the City can legally tie parking revenue to debt without a public referendum.

How Courts Distinguish a Fee From a Tax

Courts generally view a charge as a fee when it is:

Voluntary and reasonably avoidable Limited to recovering the cost of a specific service Paid only by those who directly benefit Not used for general government spending Not pledged to long-term debt

A charge begins to resemble a tax when it:

Is imposed broadly on the public Is difficult or unrealistic to avoid Generates revenue beyond cost recovery Funds general infrastructure or capital projects Is used to support borrowing Risks shifting repayment to taxpayers

How Paid Parking Fits This Framework

Paid parking in Fernandina Beach exhibits several characteristics that courts commonly associate with a tax rather than a fee.

1. It Is Not Truly Voluntary

Parking on public streets is not a discretionary luxury. For residents, workers, business owners, churchgoers, and visitors, it is a routine and often unavoidable part of daily life. When access to public right-of-way is monetized, the charge begins to resemble a compulsory payment.

2. Revenue Exceeds Cost Recovery

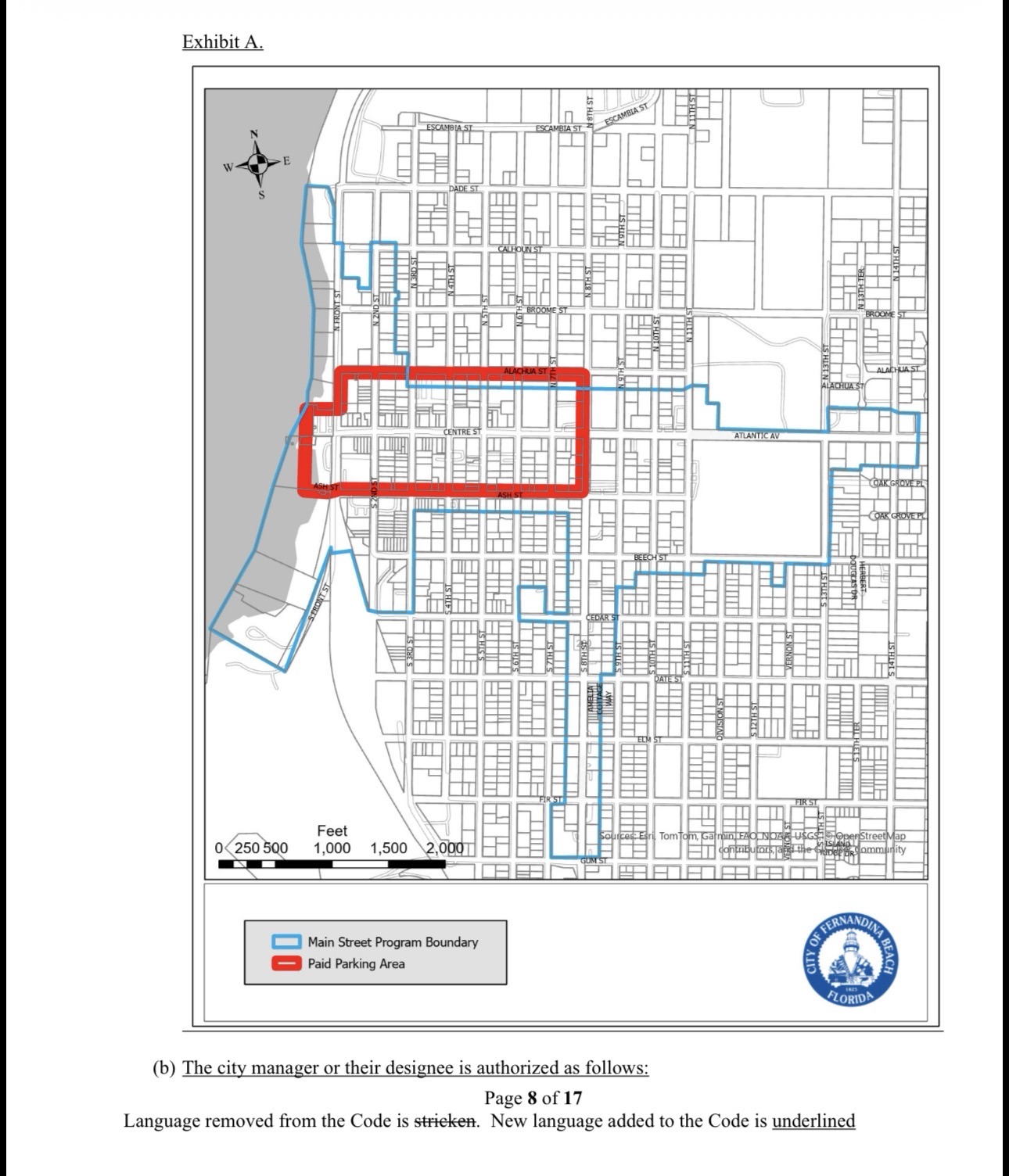

The paid parking ordinance authorizes revenue to be used for downtown infrastructure, resiliency projects, capital improvements, and debt service. That goes well beyond administering parking or managing congestion. This is revenue generation, not mere regulation.

3. Revenue Is Intended to Support Borrowing

Once parking revenue is pledged to repay debt, its function changes. It becomes a long-term funding mechanism for government projects. Courts are especially skeptical when fees are used to support borrowing without voter approval.

4. Taxpayer Backstopping Has Been Publicly Acknowledged

When an elected official publicly states that taxpayers would cover any shortfall if parking revenue fails, the argument that this is a self-contained fee weakens significantly. At that point, the risk shifts to the public at large — a hallmark of taxation.

Why This Matters Under Florida Law

Florida law allows cities to issue debt without voter approval only when:

Repayment is strictly limited to a lawful revenue source Taxpayers are fully insulated from liability No ad valorem (property tax) revenues are pledged The City’s full faith and credit are not implicated

If a court determines that paid parking:

Is compulsory in practice Generates surplus revenue Funds general government projects Supports long-term debt Exposes taxpayers to financial risk

Then it may be treated as a de facto tax, regardless of how the ordinance labels it.

What a De Facto Tax Finding Could Mean

If paid parking is ruled a de facto tax:

Borrowing authority could be invalidated Voter approval may have been required Enforcement could be delayed or enjoined Financing tied to parking revenue could be blocked

This is why the de facto tax argument carries more weight than procedural or ethics-based challenges. It attacks the foundation of the financing structure itself.

Bottom Line

A de facto tax is not about political intent or terminology. It is about how a charge operates in reality.

If paid parking functions as a compulsory charge on everyday public activity, generates surplus revenue, and exposes taxpayers to financial risk, courts may treat it as a tax — triggering voter approval requirements and limiting the City’s ability to borrow against it.

That is why this issue matters, and why it remains one of the most consequential legal questions surrounding paid parking.

AI Disclosure:

This article was prepared with the assistance of artificial intelligence for research, organization, and drafting. It is intended for informational and educational purposes only and does not constitute legal advice. Readers should independently verify facts and consult qualified legal counsel for formal legal opinions.